In a nation where the average person carries over $6,000 in credit card debt and consumer spending drives 70% of the economy, understanding why we overspend has never been more crucial. Despite our best intentions to stick to budgets and save money, many of us find ourselves repeatedly making purchases we later regret. The root of this behavior isn’t simply a lack of willpower; it’s deeply embedded in our psychology and the consumer culture that surrounds us.

Creating a Healthier Spending Habit

Our brains are wired to prioritize immediate rewards over long-term benefits, a phenomenon psychologists call “present bias.” When we see something we want, our brain’s reward system floods us with dopamine, creating a powerful urge to buy now rather than wait. This is why “Buy Now, Pay Later” services are popular among many consumers, allowing us to satisfy immediate desires while postponing financial consequences.

The digital age has amplified this tendency with one-click purchasing and same-day delivery. To combat this, try implementing a 24-hour waiting period for non-essential purchases over $50, giving your logical brain time to override emotional impulses.

When Retail Therapy Becomes a Trap

The increasing use of shopping as a form of emotional regulation is evident, with studies showing that 62% of shoppers have made purchases to improve their mood. This “retail therapy” provides a temporary mood boost but can quickly spiral into a destructive pattern.

The problem intensifies when shopping becomes our primary coping mechanism for stress, anxiety, or depression. The temporary high from making a purchase is often followed by buyer’s remorse and financial stress, creating a cycle where we spend to feel better about our previous spending. Building alternative emotional outlets, such as exercise, socialising, or creative hobbies, can help break this expensive habit.

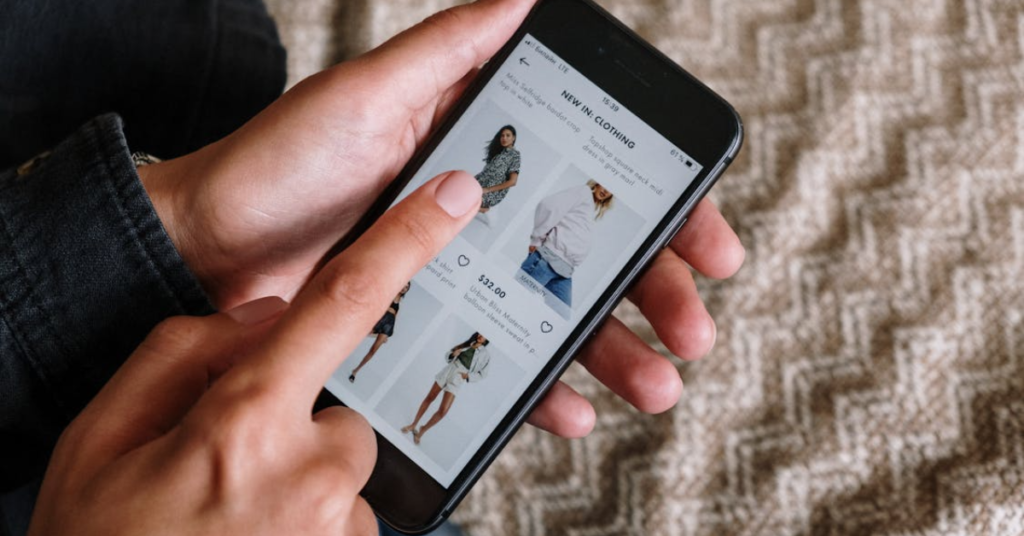

The Social Media Influence Machine

Instagram, TikTok, and Pinterest have transformed shopping from a necessity into a form of entertainment and social comparison. The rise of influencer marketing means we’re constantly exposed to curated lifestyles that make our own possessions seem inadequate.

“Haul culture” on platforms like TikTok normalises excessive purchasing, presenting it as exciting content rather than problematic behaviour. The phenomenon of “dupe culture” finding cheaper versions of expensive items might seem budget-conscious, but it often leads to buying multiple unnecessary items. Consider curating your social media feeds to reduce exposure to shopping content and unfollowing accounts that consistently promote consumerism.

Marketing Psychology and Consumer Manipulation

Retailers employ sophisticated psychological tactics designed to encourage spending. Loss aversion makes us fear missing out on “limited time” offers, even when the scarcity is artificially created. Anchoring effects make us perceive regular prices as bargains when compared to inflated “original” prices.

Retailers have perfected the art of creating urgency through countdown timers, low stock warnings, and flash sales. Store layouts are designed to maximize impulse purchases. Notice how grocery stores place candy and magazines at checkout counters. Understanding these tactics helps you recognize when your emotions are being deliberately manipulated, allowing you to make more rational purchasing decisions.

The Dangerous Allure of Credit and Easy Financing

The widespread availability of credit cards, personal loans, and buy-now-pay-later services has decoupled spending from the immediate pain of payment. When we don’t feel the financial impact right away, it’s easier to justify purchases we can’t actually afford.

This easy credit creates what economists call “payment depreciation”—the reduced psychological impact of spending money when using credit versus cash. Studies consistently show that people spend 12-18% more when using cards compared to cash. Try using the envelope method for discretionary spending categories, allocating cash amounts for entertainment, dining out, and shopping to create more awareness of your spending.

Enhancing Savings with Income Increases

As a person climbs the income ladder, they often inflate their lifestyle to match their increased earnings rather than save the difference. This “lifestyle creep” means that many high earners live paycheck to paycheck despite substantial incomes. The pressure to display success through material possessions, larger homes, luxury cars, and designer clothes keeps us trapped in spending cycles.

The concept of “keeping up with the Joneses” has evolved into keeping up with social media influencers and celebrities, setting unrealistic standards for material success. Combat lifestyle inflation by automatically increasing your savings rate whenever you receive a raise, treating future earnings as already allocated to your financial goals rather than lifestyle upgrades.

The Comparison Culture Crisis

Social media has turbocharged our tendency to compare ourselves to others, leading to what researchers call “compare and despair” spending. When we see friends’ vacation photos or colleagues’ new purchases, we often feel pressure to match their apparent lifestyle.

The curated nature of social media means we’re comparing our behind-the-scenes reality to others’ highlight reels. Remember that posts showing expensive purchases rarely include the credit card bills or financial stress that might accompany them. Focus on your own financial goals rather than trying to match others’ visible consumption.

Building Sustainable Spending Habits

Breaking free from overspending requires both psychological awareness and practical strategies. Start by identifying your personal spending triggers, whether it’s stress, boredom, social pressure, or emotional situations. Track your expenses for a month to understand your patterns without judgment.

Automate your savings so money is set aside before you can spend it, use apps that require confirmation before purchases, and practice gratitude for what you already own. Consider adopting minimalism principles or trying spending moratoriums on specific categories to reset your relationship with consumption.

Conclusion

Overspending isn’t a character flaw; it’s a natural response to psychological triggers and environmental pressures that surround consumers daily. By understanding the mental mechanics behind our purchasing decisions, we can develop more intentional relationships with money and consumption. The goal isn’t to eliminate all pleasure from spending but to ensure our financial choices align with our long-term values and goals rather than momentary impulses. With awareness and practice, it’s possible to break free from the overspending cycle and build lasting financial well-being.